What Central Florida Homebuyers Should Expect in 2026

Spring is historically the busiest season for home sales in Central Florida, and if you’re considering a purchase this year, you need numbers that reflect where the market actually stands, not where it was in 2024.

This post is built around three questions a prepared buyer would ask: What are prices doing? What does affordability actually look like when you factor in insurance, taxes, and total ownership costs? And where is the market heading through summer?

The short version: 2025 was a year of normalization. According to the Orlando Regional REALTOR Association (ORRA), the overall median home price held at $385,000, an all-time high on an annual basis, while total sales declined 5.6% year-over-year. January 2026 inventory reached 11,741 units, up 3.1% from December. ORRA president Chris Atwell characterized 2025 as a year where buyers had “more time, more options, and more room to negotiate.” Florida Realtors’ chief economist Dr. Brad O’Connor noted that monthly sales counts are rising consistently for the first time since 2022. Spring 2026 builds on that stabilization. This is a planning-year market — not a boom, not a crash — and the data supports careful action, not urgency.

Where Prices and Inventory Stand Entering Spring

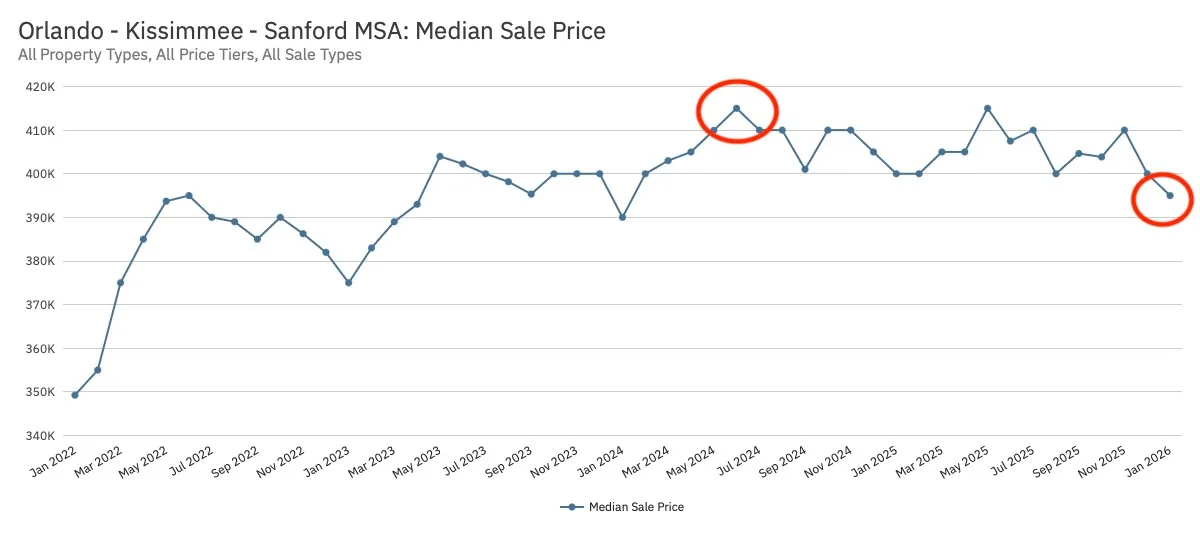

Orlando-area median home prices have pulled back modestly from the early-2024 peak of roughly $407,000 to approximately $387,000-$400,000, depending on source and month. That decline represents a correction from pandemic-era acceleration, not a crash. Prices remain elevated by historical standards, but the trajectory has shifted.

Inventory tells the more consequential story. ORRA reported January 2026 inventory at 11,741 units, with homes spending the longest average time on market since 2016. In late 2025, the Orlando market reached a 6-month supply for the first time since February 2011, the standard threshold for a balanced market.

Not all segments are moving at the same pace. In 2025, single-family home sales declined 4.4%, condo sales dropped 11.8%, and townhome sales fell 8.7%. If you’re shopping in the condo or townhome segment, you’re likely entering a softer market with more leverage than single-family buyers.

Price reductions are increasingly common. According to Houzeo, roughly 67% of Orlando listings in January 2026 had price reductions, and the sale-to-list ratio sat around 96.5%. That gap between asking price and sale price gives buyers negotiation room that simply didn’t exist during 2021-2023. The seasonal uptick in new listings typically accelerates through March-May, so additional inventory is expected, though not a flood.

The chart below shows how Orlando-area median home prices have moved since 2022:

What Mortgage Rates and Total Ownership Costs Look Like Right Now

Mortgage rates have improved meaningfully from 2023-2024 highs. As of early March 2026, the average 30-year fixed rate in Florida sits around 5.75%-5.94%, depending on source, down from the 6.8%+ environment of early 2025 and the 7%+ peaks of 2023. Bankrate reported the Florida average at 5.94% on March 2, 2026, while CBS News and Zillow placed the national average 30-year fixed at 5.75%.

The Fed cut rates three times in late 2025. The next FOMC meeting is scheduled for March 17-18, 2026, though odds of an additional cut appear low. The practical takeaway: plan around current rates, not forecasted ones.

However, the mortgage payment is only one line item. In Central Florida, total cost of ownership extends well beyond principal and interest. Florida homeowners insurance averages roughly $3,800-$5,600 annually statewide, depending on coverage level. The Florida Office of Insurance Regulation reported an average annual premium of approximately $3,815 with wind coverage, up about 6% year-over-year, but significantly slower than the double-digit annual increases of prior years. Citizens Property Insurance announced a statewide average 8.7% premium reduction for spring 2026 renewals, a meaningful development for buyers concerned about insurance costs.

Property taxes, HOA fees (especially for condos and townhomes), and flood insurance where applicable must be factored into monthly budgets. Many first-time buyers underestimate these line items by 20-30%. Florida’s lack of a state income tax helps offset some ownership costs for buyers relocating from high-tax states, but that advantage is partially consumed by insurance and property tax obligations.

Here’s what a monthly budget might look like for a $385,000 home at two different rate scenarios, assuming 5% down:

| 5.75% Rate | 6.50% Rate | |

|---|---|---|

| Home Price | $385,000 | $385,000 |

| Down Payment (5%) | $19,250 | $19,250 |

| Loan Amount | $365,750 | $365,750 |

| Mortgage (P&I) | $2,135/mo | $2,312/mo |

| Property Tax (est.) | $385/mo | $385/mo |

| Homeowners Insurance | $350/mo | $350/mo |

| PMI (est.) | $150/mo | $150/mo |

| HOA (if applicable) | $75-$300/mo | $75-$300/mo |

| Total Monthly Cost | $3,095-$3,320/mo | $3,272-$3,497/mo |

| Rate Difference | — | +$177/mo |

Estimates based on 1.2% property tax rate, ~$4,200/year insurance (statewide midpoint), and 0.5% annual PMI. HOA varies by property type. Consult a lender and insurance agent for quotes specific to your situation.

For eligible buyers, the Florida Housing First-Time Homebuyer Program offers low-interest loans and up to $10,000 in down payment assistance through the Florida Assist program, worth exploring before assuming you need 20% down.

What “Balanced Market” Means for Buyers This Spring

A balanced market, roughly 5-6 months of supply, means neither buyers nor sellers hold dominant leverage. ORRA data shows the Orlando market reached 6.43 months of supply in November 2025, the first balanced reading since February 2011. For buyers, that translates into practical advantages that weren’t available during the pandemic years.

You can negotiate on price, closing costs, and repairs. You can request an inspection contingency without getting passed over. You can take a week to evaluate a property before making an offer. With an average of 77+ days on market in January 2026, the panic-bidding dynamic of 2021-2023 is gone.

That said, the market is balanced in aggregate but competitive in pockets. Homes in desirable locations (strong school zones, recent renovations, move-in ready condition, pools, larger lots) will still move faster and attract stronger offers. Popular Orlando-area suburbs like Lake Nona, Winter Garden, Windermere, Winter Park, and Dr. Phillips continue to see healthy demand, particularly from relocating professionals. Seminole County communities offer relative affordability and strong school ratings within commuting distance of Orlando.

Contingency offers (inspection, financing, and even sale contingencies) are becoming more common again. Sellers who need to close before buying may accept terms that were non-starters two years ago. Pending sales surged 18.7% from October to November 2025, signaling that pent-up demand is converting into activity as conditions improve.

How to Use This Information Before You Start Touring Homes

Data is only useful if it changes how you prepare. Here are four steps worth taking before the spring inventory wave peaks:

- Get pre-approved, not just pre-qualified. Pre-approval gives you a verified budget and signals seriousness to sellers in a market where negotiation matters.

- Run a total-cost-of-ownership calculation. Request insurance quotes for your target price range. Estimate property taxes and HOA fees. Build a monthly budget that reflects actual ownership costs, not just the mortgage payment.

- Narrow your geography. Identify 2-3 target neighborhoods based on your commute, priorities, and budget. Price ranges, school quality, insurance costs, and flood zone designations can vary block by block. Research specific areas rather than the Orlando metro broadly.

- If relocating, budget a scouting trip. Online research is essential but doesn’t replace physically experiencing commute times, neighborhood character, and proximity to daily needs.

One additional note: metro-wide median price statistics don’t tell you what’s happening in your price range or preferred zip codes. Ask a local agent for ORRA data specific to your target areas. The difference between a zip code trending up and one trending flat can meaningfully affect your negotiating position and long-term outlook.

For eligible buyers, the My Safe Florida Home program offers wind mitigation inspections and grants that can reduce insurance premiums over time, a detail worth investigating early in the process.

Conclusion

Key Takeaways:

- Orlando-area home prices have softened from 2024 peaks while remaining near record annual levels. Inventory is the highest it’s been in over a decade, giving buyers time and options.

- Mortgage rates in the mid-to-upper 5% range represent a meaningful improvement from 2023-2024, but total ownership costs, especially insurance, require careful budgeting beyond the mortgage payment.

- The market is balanced for the first time since 2011. Buyers can negotiate on price, contingencies, and closing costs in ways that weren’t possible during the pandemic years.

- Preparation matters more than speed. Pre-approval, total-cost analysis, and neighborhood-level research are the highest-value steps before touring homes.

Spring 2026 in Central Florida is a market that rewards preparation, not urgency. Conditions are more favorable for buyers than at any point since before the pandemic, but the advantage goes to those who’ve done the work on total costs, target neighborhoods, and financing. The data supports careful, informed action — and the best time to start that preparation is before the spring inventory wave peaks.

Want the latest market report for your target zip code or neighborhood? I’ll send you a free market snapshot so you can compare it against what you’ve read here.